This by Hisham Farag and David Dickinson

Why Climate Finance?

Recent episodes of environmental disasters such as wildfires, typhoons and droughts provide evidence of the catastrophic economic impact of climate change. These events have a devastating impact on infrastructure, natural habitats and have inflicted suffering on our collective wellbeing. The climate crisis is therefore an immediate existential threat. The former Bank of England governor and the UN envoy for climate action and finance, Mark Carney, has warned that the climate crisis potential death toll could, by far, exceed the Covid-19 pandemic. The estimated annual cost of natural disasters caused by climate change is about $18 billion in low and middle-income countries and $390 billion to companies and households worldwide.

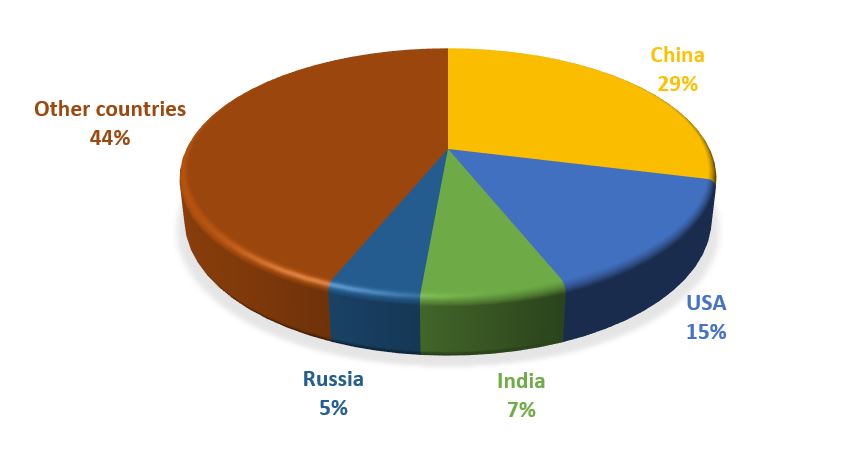

The extensive burning of fossil fuels is the primary source of greenhouse gases emissions. Transportation, electricity production, and manufacturing sectors accounts for the larger proportion of emissions that traps the heat in the atmosphere and causes global warming. Global warming, in turn, has led to even greater demand on energy; the world energy consumption in 2019 was roughly 584 exa-Joule (this is equivalent to powering 27 light bulbs of 50W each for 13.8 billion years). This, indeed, has implications for financial sector to fund the transition to greener economies to combat the impact of global warming. Figure 1 presents the CO₂ emission in 2019; the top 4 emitters account for 56% of CO₂ emission while the rest of the world account for 44%.

Figure 1: Mt CO₂ emission in 2019

Figure 1: Mt CO₂ emission in 2019

Source: Global Carbon Project

Recognising the important role of the financial sector in combatting climate change, HM Treasury and the Department for Business, Energy & Industrial Strategy, in 2019, published the UK Green Finance Strategy. This aims at greening financial systems by focussing financial market attention on investments that contribute to a major transformation to clean and resilient economic growth. The Green Finance Institute (GFI) was created as part of this policy initiative with a remit to achieve an inclusive, net-zero carbon and resilient economy.

To bridge the funding gap, financial markets are moving in a positive direction to deliver sustainable greener economies. Funding the transition to sustainable low-carbon economies is a challenge that needs solidarity from the international community. Climate Finance is therefore an important part of the international drive to achieve a solution to the problem of Climate Change.

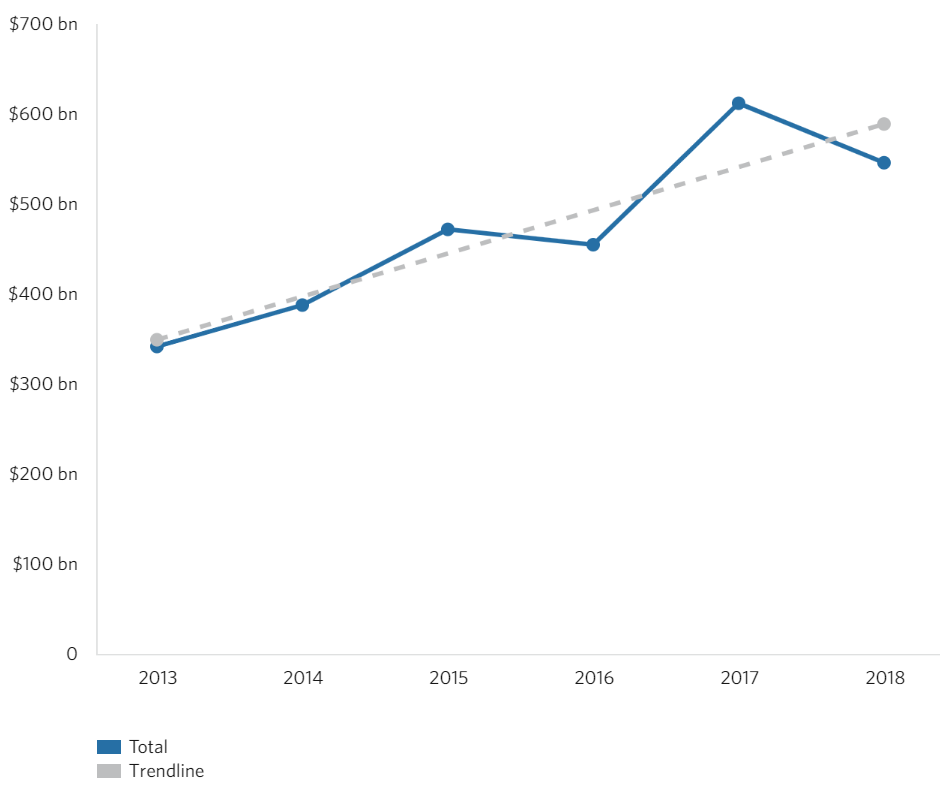

Financial institutions worldwide, prompted by their own risk assessments, by investors, as well as by Regulators, are developing innovative sources of finance that have led to the rise of “Climate Finance”; The UNFCCC defines climate finance as “local, national or transnational financing—drawn from public, private and alternative sources of financing—that seeks to support mitigation and adaptation actions that will address climate change”. Figure 2 shows that the annual climate finance flows exceeded USD half-trillion mark for the first time in 2018 and clearly will grow further over the coming decade to meet the global environmental challenges.

Figure 2: Total Global Climate Finance Flows 2013-2018

Figure 2: Total Global Climate Finance Flows 2013-2018

Source: Climate Policy Initiative

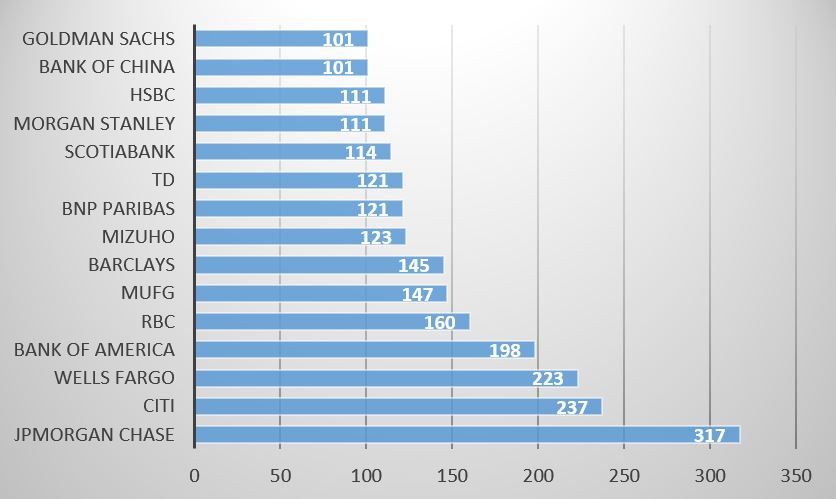

However, this is a drop in the ocean compared with the funding provided to fossil fuel-based projects. During the five years, post Paris Accord, the top 60 banks worldwide poured $3.8 trillion into fossil fuels-based projects. Figure 3 presents the top 15 banks financing fossil fuels projects globally, 2016 – 2020.

Figure 3: Top 15 banks financing fossil fuels globally, 2016 – 2020 (US Billions)

Source: Banking on Climate Chaos Report, 2021

The challenges facing the global economy are clear from these relative funding figures and the changes in production and consumption that are required are similarly huge. Financial markets and institutions will need to develop green finance as a matter of urgency in order to provide the finance required to deliver the necessary shift to a green economy. Therefore, financial innovation is bound to be a key mechanism for delivering sustainable economic structures.

Innovation in Financial Markets

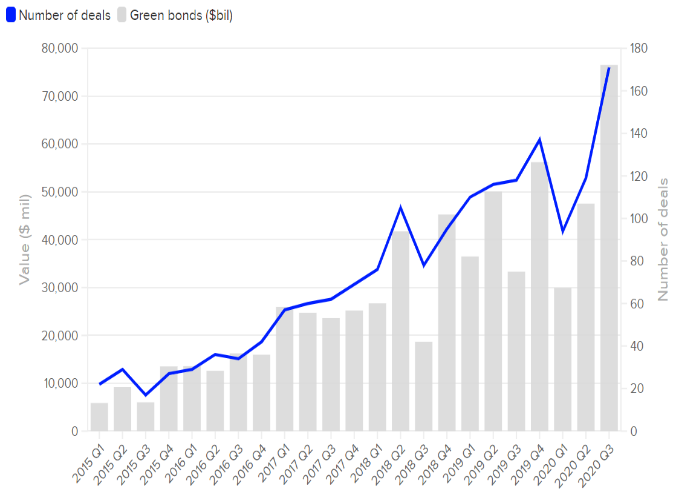

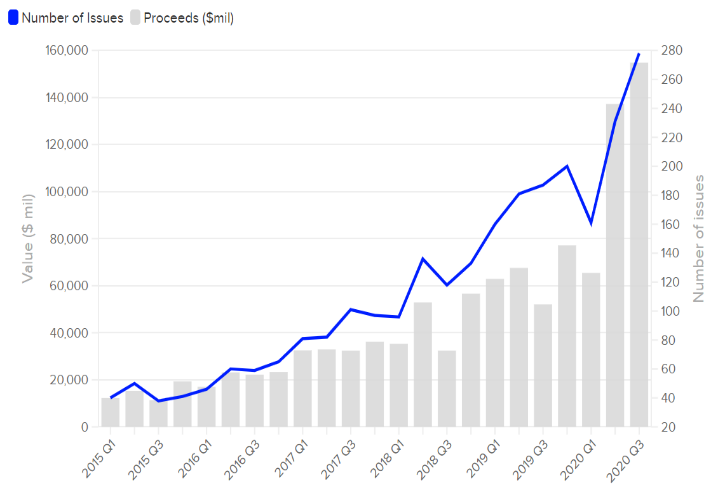

Financial innovation has the power to significantly change the landscape of finance available for businesses. The creation of Green, Blue and Social/Sustainability Bonds is one example of financial innovation that has delivered funding to support the response to climate change. The proceeds of Green Bonds are committed to finance climate friendly projects while the proceeds of Blue Bonds are devoted to fund sustainable marine and ocean-based initiatives. These innovations are non-mutually exclusive types; for instance, Social Bonds could be common ordinary Bonds but with proceeds directed to environmentally friendly projects. The cumulative market value of Green Bonds issuance to date is US$1.185tn. In 2019, Fannie Mae - the US Federal National Mortgage Association – issued the largest amount of Green Mortgage Backed Securities (US$22.8bn). And HSBC has recently announced their global commitment to provide $100 billion in sustainable financing and investment by 2025. Figures 4 and 5 present the quarterly global Green and Sustainability Bonds issuance up to the third quarter of 2020.

Figure 4: Quarterly Global Green Bonds

Source: Refinitiv Deals Intelligence

Figure 5: Sustainable Bonds Quarterly Volumes

Source: Refinitiv Deals Intelligence

But there is much more to do in terms of financial markets development, instruments, and regulations to achieve the required switch to green investing. In the wake of its commitments to reach net zero carbon emissions by 2050, the UK is the first country to set out plans to issue the first ever Sovereign Green Bond while the Republic of Seychelles was first to issue sovereign Blue Bonds worth US$15 million in October 2018. Morgan Stanley, in collaboration with the World Bank, issued $10 million worth of Blue Bonds to clear plastic pollution in the ocean and The Nature Conservancy announced an ambitious plan to issue $1.6 billion worth of Blue Bonds by 2025. More funding will be required in the wake of the Japanese government’s recent decision to release 1.23 million tons of radioactive contaminated water from the Fukushima nuclear plant into the Pacific Ocean.

Green or Blue Bonds issuance sends a strong positive signal to stakeholders on a company’s commitments towards undertaking environmentally friendly projects. However, companies may issue such innovative Bonds to improve their image “greenwashing” or to benefit from the use of cheaper finance. A recent study finds that the two main motivations for investors to hold socially responsible mutual funds are social preferences and social signalling and that financial motives are not the main driver for socially responsible investments (SRI) decisions.

Financial Markets Implications

Beyond the creation of new financial products, uncertainty about the economic impact of climate change, pricing and hedging for climate risk, further complicates the estimation of risk premia and the overall social cost of climate change. It is becoming clear that carbon emission has implications for stock markets; a recent study finds that higher carbon emission leads to lower valuation of US companies. Another study found evidence of “carbon exposure premium” as the required rate of return for companies with high carbon emission exceeds those with lower emission. Carbon Pricing is a key policy followed by 46 national jurisdictions – as of November, 2019 – to address climate change. Such initiatives will have an impact on the cost of capital and companies with high levels of carbon emission will have lower market values consequently.

However, the imposition of carbon taxes could have unintended consequences for the energy sector, such as fossil fuel stranded assets. Climate risks, in particular regulatory risk, also have implications for portfolio construction and asset allocations. Fund managers, as a result of increasing pressure from stakeholders, incorporate Environment, Social and Governance (ESG) criteria into their portfolios. A study found that incorporating ESG criteria into investment decision could reduce portfolio risk.

The economic implications of climate change have been investigated in fixed income securities markets. For instance, Green Bonds are found to offer, on average, lower yields (since they are issued at a premium). However, a recent study investigated whether investors are willing to sacrifice higher yields for societal benefits and found no difference in the pricing of Green and non-Green bonds; this implies that the greenium is zero. This result varies across countries as those impacted by climate change are expected to pay higher underwriting fees and higher premiums on long-term municipal bonds reflecting the higher risks associated with climate change that they face. Overall, stock markets are found to react positively to the issuance of Green Bonds.

Climate change also has implications for the real estate sector; sea level rise and flooding riskea level rise and flooding risk are obvious examples that have clear economic impact, for example the impact of Hurricane Sandy in 2012 on property prices in New York City. The long-term impact of climate risk has been investigated. A study found that by the year 2100 around 13.1 million Americans will be impacted if the sea level rises by 1.8 metres; another study estimates that about 1.9 million houses worth of $882 billion, mainly in Florida, will be at risk of flooding if the sea level rises by six feet. A recent study found that houses exposed to rising sea levels are sold on average 7% less than unexposed properties. Awareness of global warming is increasing; a study found that where local temperatures are abnormally high, the volume of Google searches for “global warming” is increasing across different cities around the world.

Hedging against climate risk is a key challenge for financial markets as the existing derivatives instruments and specialised insurance products typically do not cover the long-term impact of climate risk. A recent study designed an alternative approach to hedge against climate risk by designing a “climate news” index using the WSJ coverage of climate change news. While, climate-resilient assets will continue their growth, empirical research will need to inform decision-makers and regulatory bodies about improved measures of companies’ climate risk. This will spur financial innovation to develop appropriate techniques for hedging against climate risk, the social cost of carbon emissions, and the impact of climate risk on financial stability.

Disclosure and Shareholder Activism

Although, voluntary disclosure is an essential step towards greater transparency on climate risks, a policy intervention is required to make such disclosure mandatory. The UK is the first country to establish a Task Force on Climate-related Financial Disclosures (TCFD) which aims to make disclosures fully mandatory across the economy by 2025, going beyond the ‘comply or explain’ approach. While the US Securities and Exchange Commission (SEC) regularly assesses how current climate change disclosures adequately inform investors, the U.S. climate envoy, John Kerry, recently highlighted that President Biden is set to issue an executive order on climate disclosure in capital markets.

Since financial markets are global there has been a push towards standardisation of regulation and supervision. The British Standard Institute (BSI) has developed a set of standards for financial institutions to align with the global sustainability challenges and to promote the UK Green Finance strategy. The Climate Bonds Initiative (CBI) published its Climate Bonds Standard and Certification Scheme in 2010 and the International Capital Markets Association (ICMA), introduced the principles of green loans in 2014 as voluntary initiatives.

Stakeholders also play a fundamental role in shaping corporate culture and raising awareness of the ESG and SRI investing; the United Nations-backed Principles of Responsible Investments (PRI) and the promote the importance of incorporating environmental, social and corporate governance issues into investment practices. ESG assets under management have a value of around US$40.5 trillion, which is equivalent to one third of all professionally managed assets. Shareholder activists continue to put pressure on boards to undertake voluntary disclosure of the potential impact of climate change and its risk mitigation measures. A recent study found that shareholder activists play an essential role in influencing companies to disclose climate change risks voluntarily. The study also found that stock markets react positively to climate-related disclosure. Shareholders of BP, Exxon Mobil, Occidental Petroleum, and PPL Corporation agreed proposals to disclose on the risks of climate change. However, recently, the board of Berkshire Hathaway unanimously recommended shareholders vote against a proposal to disclose the company’s climate risk management approach.

There is a large strand of literature that considers how to align directors’ interests with wider stakeholder interests to combat the impact of climate change. In 2009, the Business Roundtable in the US redefined the purpose of corporations in a statement signed by 181 CEOs that required them to commit to lead their companies for the benefit of all stakeholders. A recent study found that aligning executive compensation to ESG criteria leads to an increase in social and environmental initiatives. Another study found that 51% of S&P 500 companies incorporate ESG metrics (mostly subjective) in their incentive plans. In the UK, 45% of FTSE100 companies incorporate ESG measures into their executive incentive plans.

Concluding Remarks

Although, most countries have committed to reach net zero carbon emissions by 2050, the current political landscape and the impact of the Covid-19 pandemic could influence implementation plans. Recently, the UK, EU and the US have committed to a substantial cut (50% - 68%) in carbon emissions by 2030. However, India as one of the top carbon emitters see the 2050 net zero target as a “pie in the sky”. This could lead to “free riding problems”; a recent study argued that countries that are not taking serious measures towards reducing greenhouse gas emissions will benefit if other countries do reduce their emissions. The study emphasises the need to establish a governing body with clear responsibility to ensure all countries deliver on their climate commitments.

The rapid growth in financial technology casts doubt on achieving the net-zero carbon by some countries. The world electricity consumption for Bitcoin in 2019 was 126.07 terawatt-hours (TWh). This is higher than the total energy consumption in Norway (124.13 TWh per year) or Argentina (125.03 TWh per year). A recent study reported that, in April 2020, 75% of the world’s cryptocurrencies mining is found in China and that the growth in crypto assets and blockchain activities is expected to generate 130.50 million metric tons of carbon emissions by 2024.

While Sustainable Finance will continue its growth, academics and practitioners are facing challenges to set out a new research agenda including important policy questions about risk and return profiles and premiums (the greenium) of green financial assets particularly in the context that the risks associated with climate change are very long term. In addition, there are questions to be answered about the objectives of investors who hold green assets. For instance, why do investors sacrifice a reasonably high rate of return on conventional bonds and invest in a lower rate of return on sustainable bonds? Disclosure on climate risks also presents different perspectives in the context of market reaction; the results of academic research reveal that voluntary disclosure leads to a positive stock market reaction as investors value transparency. Regulatory bodies are often required to continue to raise the disclosure bar until mandatory disclosure is in place. Further research is needed to understand the costs and benefits of regulation in respect to climate change. For example, there are unintended consequences of addressing climate change risks. In Jan 2021 the market value of energy companies listed on S&P500 dropped by 12% compared with market value in Jan 2020. The growth in sustainability-based investments, together with divestment campaigns by stakeholders, has led some fund managers to screen out polluting companies from their portfolios. This may be welcomed as a market response to climate risk, but it is unclear what the long-term impact of such market moves will be. Given that the market capitalisation of the biggest ten energy companies worldwide by the end of 2020 was about US$2.2trilion, it could lead to a substantial stranded assets risk and a potential systemic risk.

We conclude with a set of recommendations for policy debate. First, company boards should think strategically about their wider stakeholders and align shareholder value with stakeholder value. Second, regulatory changes should be made to tax negative externalities and to raise the disclosure bar leading to a mandatory disclosure on climate related risk and its mitigation measures, and to design an international mechanism by which a fair climate finance contribution by top emitters is achieved. Third, international collaboration should be established to accelerate the transitions towards clean energy and to put measures in place to mitigate any unintended consequences of that transition. Fourth, there should be a clear strategy from financial institutions and markets to develop financial products and institutions that can assist in the process of moving to a sustainable economy. This includes the creation of financial assets that fund the real sector developments that will stop global warming and, more generally, prevent damage to the environment. Finally, we should recognise that economies and financial sectors may need to move at different speeds and the role of international agencies in achieving a balance across developed and developing economies is important in this regard.